Extract coefficients from an adaptive PENSE (or LS-EN) regularization path with hyper-parameters chosen by cross-validation.

Usage

# S3 method for class 'pense_cvfit'

coef(

object,

alpha = NULL,

lambda = "min",

se_mult = 1,

sparse = NULL,

standardized = FALSE,

...

)Arguments

- object

PENSE with cross-validated hyper-parameters to extract coefficients from.

- alpha

Either a single number or

NULL(default). If given, only fits with the givenalphavalue are considered. Iflambdais a numeric value andobjectwas fit with multiple alpha values and no value is provided, the first value inobject$alphais used with a warning.- lambda

either a string specifying which penalty level to use (

"min","se","{m}-se") or a single numeric value of the penalty parameter. See details.- se_mult

If

lambda = "se", the multiple of standard errors to tolerate.- sparse

should coefficients be returned as sparse or dense vectors? Defaults to the sparsity setting of the given

object. Can also be set tosparse = 'matrix', in which case a sparse matrix is returned instead of a sparse vector.- standardized

return the standardized coefficients.

- ...

currently not used.

Value

either a numeric vector or a sparse vector of type

dsparseVector

of size \(p + 1\), depending on the sparse argument.

Note: prior to version 2.0.0 sparse coefficients were returned as sparse matrix of

type dgCMatrix.

To get a sparse matrix as in previous versions, use sparse = 'matrix'.

Hyper-parameters

If lambda = "{m}-se" and object contains fitted estimates for every penalization

level in the sequence, use the fit the most parsimonious model with prediction performance

statistically indistinguishable from the best model.

This is determined to be the model with prediction performance within m * cv_se

from the best model.

If lambda = "se", the multiplier m is taken from se_mult.

By default all alpha hyper-parameters available in the fitted object are considered.

This can be overridden by supplying one or multiple values in parameter alpha.

For example, if lambda = "1-se" and alpha contains two values, the "1-SE" rule is applied

individually for each alpha value, and the fit with the better prediction error is considered.

In case lambda is a number and object was fit for several alpha hyper-parameters,

alpha must also be given, or the first value in object$alpha is used with a warning.

See also

Other functions for extracting components:

coef.pense_fit(),

predict.pense_cvfit(),

predict.pense_fit(),

residuals.pense_cvfit(),

residuals.pense_fit()

Examples

# Compute the PENSE regularization path for Freeny's revenue data

# (see ?freeny)

data(freeny)

x <- as.matrix(freeny[ , 2:5])

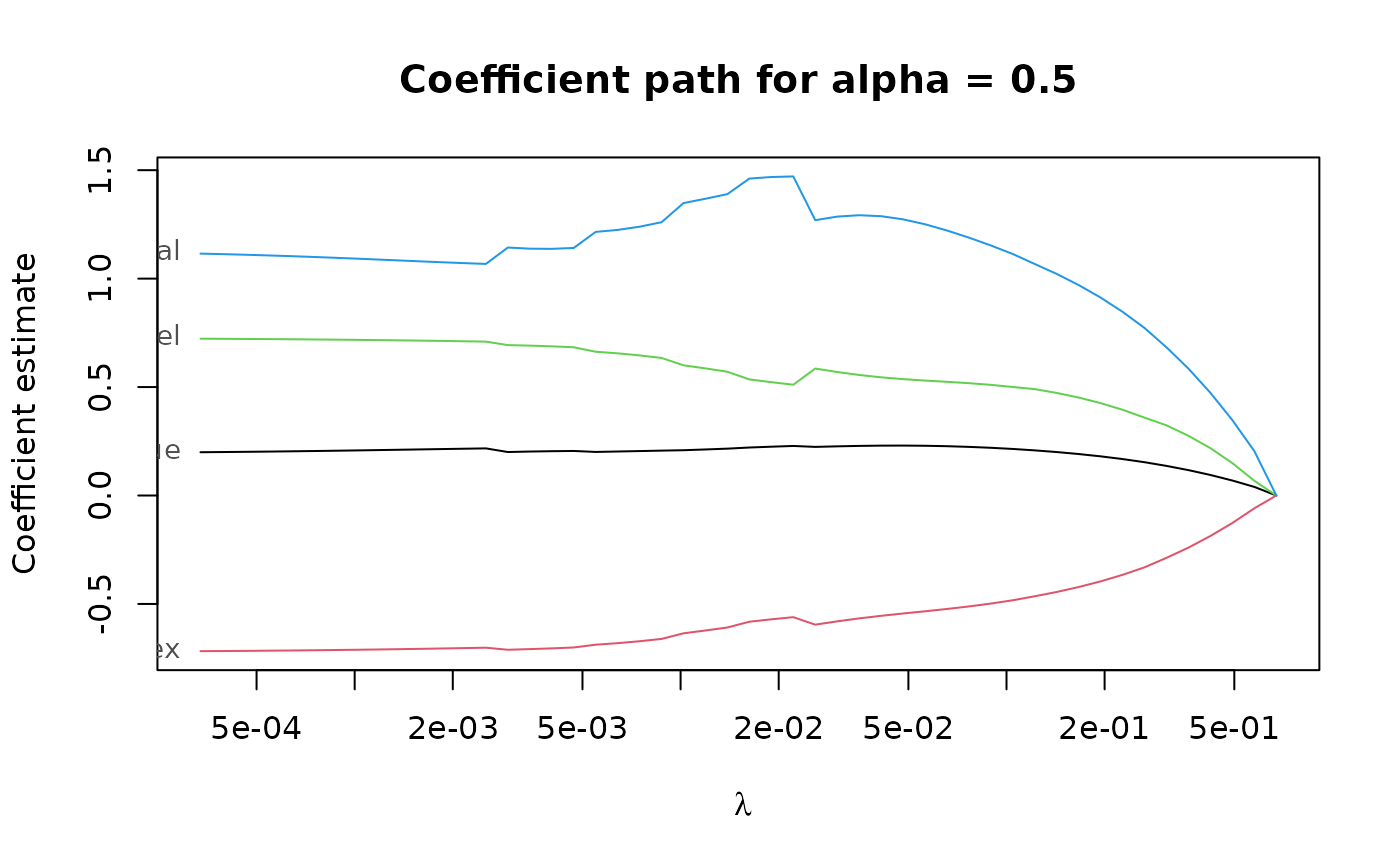

regpath <- pense(x, freeny$y, alpha = 0.5)

plot(regpath)

# Extract the coefficients at a certain penalization level

coef(regpath, lambda = regpath$lambda[[1]][[40]])

#> (Intercept) lag.quarterly.revenue price.index

#> -6.5082299 0.2510560 -0.6879670

#> income.level market.potential

#> 0.7090986 0.9409940

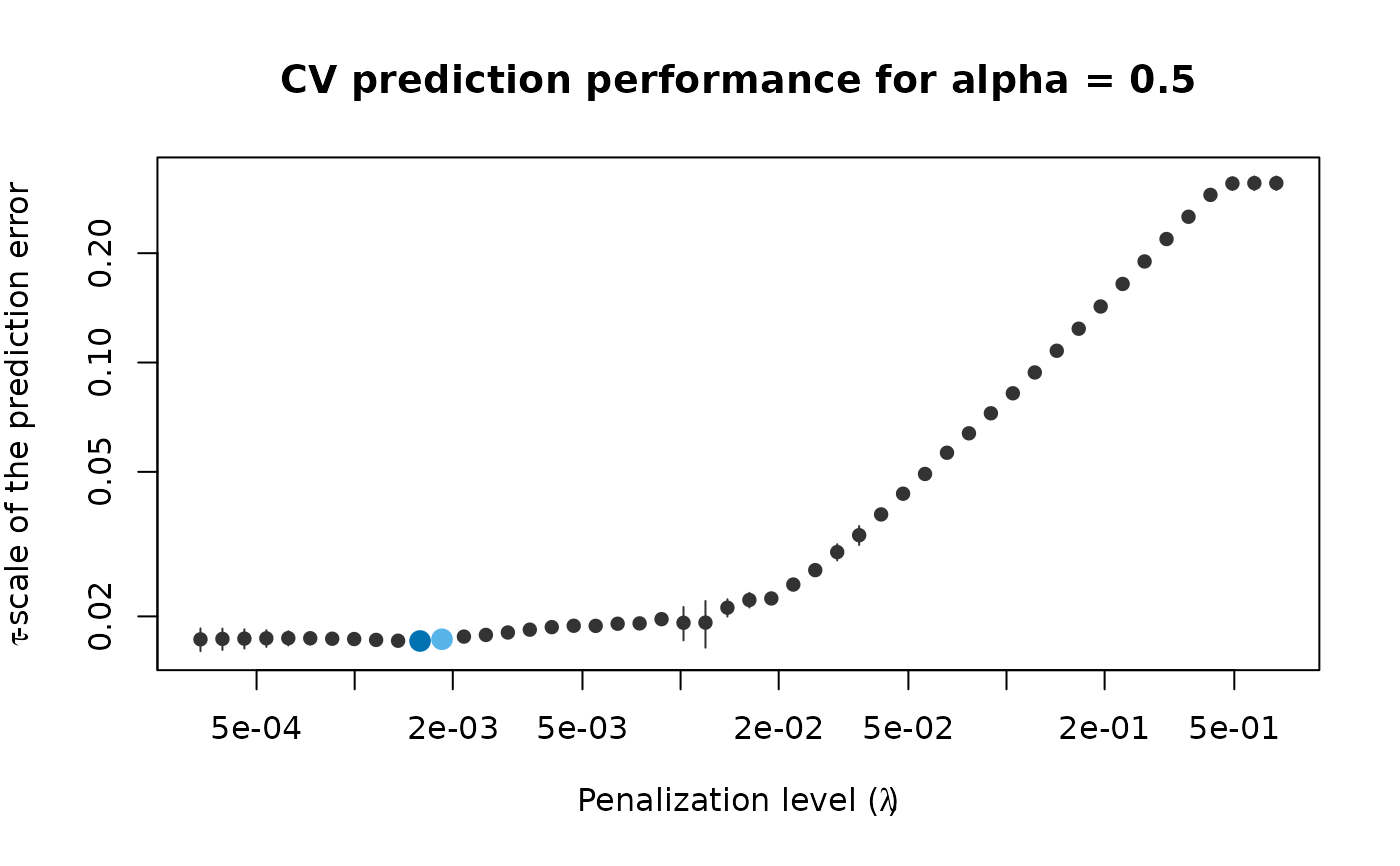

# What penalization level leads to good prediction performance?

set.seed(123)

cv_results <- pense_cv(x, freeny$y, alpha = 0.5,

cv_repl = 2, cv_k = 4)

plot(cv_results, se_mult = 1)

# Extract the coefficients at a certain penalization level

coef(regpath, lambda = regpath$lambda[[1]][[40]])

#> (Intercept) lag.quarterly.revenue price.index

#> -6.5082299 0.2510560 -0.6879670

#> income.level market.potential

#> 0.7090986 0.9409940

# What penalization level leads to good prediction performance?

set.seed(123)

cv_results <- pense_cv(x, freeny$y, alpha = 0.5,

cv_repl = 2, cv_k = 4)

plot(cv_results, se_mult = 1)

# Print a summary of the fit and the cross-validation results.

summary(cv_results)

#> PENSE fit with prediction performance estimated by 2 replications of 4-fold ris

#> cross-validation.

#>

#> 4 out of 4 predictors have non-zero coefficients:

#>

#> Estimate

#> (Intercept) -4.7921541

#> X1 0.3338834

#> X2 -0.6140406

#> X3 0.6954769

#> X4 0.7316339

#> ---

#>

#> Hyper-parameters: lambda=0.0003364066, alpha=0.5

# Extract the coefficients at the penalization level with

# smallest prediction error ...

coef(cv_results)

#> (Intercept) lag.quarterly.revenue price.index

#> -4.7921541 0.3338834 -0.6140406

#> income.level market.potential

#> 0.6954769 0.7316339

# ... or at the penalization level with prediction error

# statistically indistinguishable from the minimum.

coef(cv_results, lambda = '1-se')

#> (Intercept) lag.quarterly.revenue price.index

#> -11.4754472 0.2265866 -0.5739724

#> income.level market.potential

#> 0.5417608 1.3768215

# Print a summary of the fit and the cross-validation results.

summary(cv_results)

#> PENSE fit with prediction performance estimated by 2 replications of 4-fold ris

#> cross-validation.

#>

#> 4 out of 4 predictors have non-zero coefficients:

#>

#> Estimate

#> (Intercept) -4.7921541

#> X1 0.3338834

#> X2 -0.6140406

#> X3 0.6954769

#> X4 0.7316339

#> ---

#>

#> Hyper-parameters: lambda=0.0003364066, alpha=0.5

# Extract the coefficients at the penalization level with

# smallest prediction error ...

coef(cv_results)

#> (Intercept) lag.quarterly.revenue price.index

#> -4.7921541 0.3338834 -0.6140406

#> income.level market.potential

#> 0.6954769 0.7316339

# ... or at the penalization level with prediction error

# statistically indistinguishable from the minimum.

coef(cv_results, lambda = '1-se')

#> (Intercept) lag.quarterly.revenue price.index

#> -11.4754472 0.2265866 -0.5739724

#> income.level market.potential

#> 0.5417608 1.3768215